BUSINESS

Fixed Deposit Rates Compared: Which Offers Better Returns in July 2026—HDFC, ICICI, Kotak, or AU Small Finance Bank?

With inflation continuing to impact household expenses, many investors are looking for safe investment options that provide predictable returns. Among the various choices available, Fixed Deposits (FDs) remain one of the most trusted investment instruments because they offer guaranteed interest and protect investors from market volatility.

Unlike stocks or mutual funds, where returns depend on market performance, fixed deposits provide a predetermined interest rate for a specified tenure. This allows investors to know their expected maturity amount in advance, making FDs particularly attractive for conservative investors, salaried employees, retirees, and individuals seeking capital protection.

Here's a comparison of the fixed deposit interest rates and key features offered by HDFC Bank, ICICI Bank, Kotak Mahindra Bank, and AU Small Finance Bank.

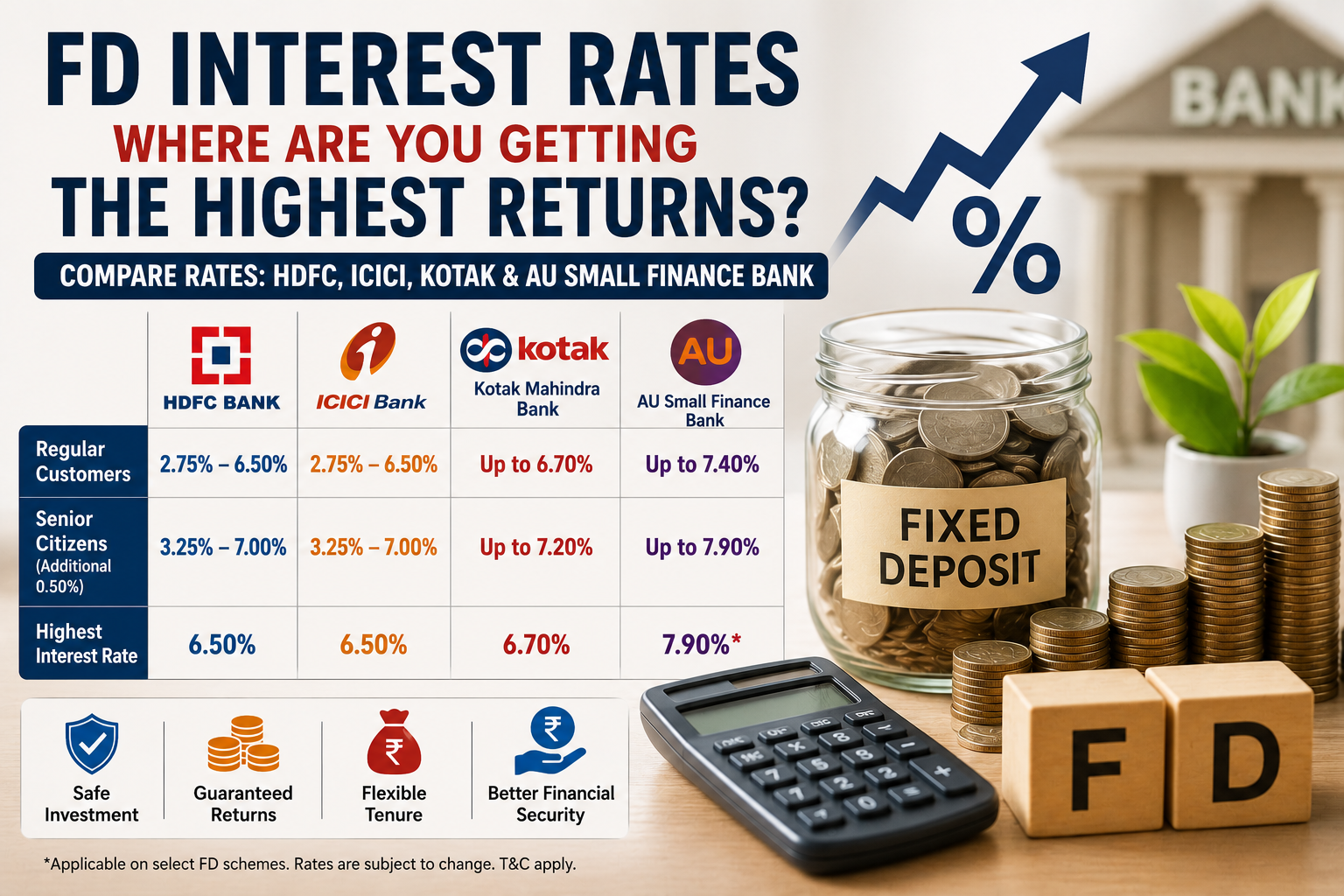

HDFC Bank Fixed Deposit Interest Rates

HDFC Bank continues to offer competitive returns across various FD tenures.

As of July 2026:

-

Regular customers: Interest rates range from 2.75% to 6.50% per annum.

-

Senior citizens: Eligible for an additional 0.50% annual interest over the standard rates.

The bank also periodically introduces special tenure fixed deposits, which may offer slightly higher returns than regular FD schemes for selected investment periods, typically ranging between 18 months and three years.

These special deposits can be an attractive option for investors seeking improved returns without taking additional risk.

ICICI Bank Fixed Deposit Rates

ICICI Bank offers interest rates similar to several leading private banks.

Current FD rates include:

-

Regular customers: 2.75% to 6.50% per annum.

-

Senior citizens: Additional 0.50% annual interest over regular rates.

Apart from fixed deposits, the bank also provides the iWish feature, a flexible recurring deposit facility.

Unlike traditional recurring deposits that require deposits on fixed monthly dates, iWish allows customers to invest whenever funds are available, making it suitable for freelancers, self-employed professionals, and individuals with irregular monthly income.

Kotak Mahindra Bank FD Rates

Kotak Mahindra Bank currently offers one of the higher FD rates among large private sector banks.

-

Regular customers: Interest rates up to 6.70% per annum.

-

Senior citizens: Eligible for an additional 0.50% interest.

The bank also offers an automatic sweep facility known as ActivMoney.

Under this feature, surplus funds maintained in a savings account above a predefined threshold are automatically transferred into fixed deposits. Whenever money is required, the system can move eligible funds back into the savings account automatically, allowing customers to earn higher returns while retaining liquidity.

AU Small Finance Bank Offers Higher Interest Rates

Among the banks compared, AU Small Finance Bank currently provides some of the highest fixed deposit returns.

According to the available information:

-

Regular customers: Interest rates up to 7.40% per annum.

-

Senior citizens: Additional 0.50% annual interest.

Certain special fixed deposit schemes may offer returns of up to 7.90%, depending on tenure and applicable conditions.

The bank also offers the Planet First – AU Green Fixed Deposit, a specialized product designed for customers interested in supporting environmentally focused initiatives alongside their investments.

Factors to Consider Before Choosing an FD

Although interest rate is an important consideration, investors should evaluate several other factors before opening a fixed deposit.

These include:

-

Financial strength and reputation of the bank.

-

Premature withdrawal rules and penalties.

-

Available investment tenures.

-

Auto-renewal options.

-

Frequency of interest payouts.

-

Deposit insurance coverage.

-

Customer service and digital banking facilities.

Selecting an FD based solely on the highest interest rate may not always be the best long-term decision.

Cumulative vs Non-Cumulative Fixed Deposits

Banks generally offer two types of fixed deposits.

Cumulative Fixed Deposits reinvest the earned interest throughout the investment period. Investors receive both principal and accumulated interest together at maturity.

Non-Cumulative Fixed Deposits pay interest at regular intervals such as monthly, quarterly, half-yearly, or annually, making them suitable for individuals seeking periodic income.

Tax Saver Fixed Deposits

Investors looking for tax-saving opportunities may consider Tax Saver Fixed Deposits.

Key features include:

-

Mandatory lock-in period of five years.

-

Eligible for tax deduction under Section 80C of the Income Tax Act, subject to applicable limits.

-

Interest rates generally range between 6.25% and 7.90%, depending on the bank.

Since premature withdrawal is not permitted during the lock-in period, investors should consider their liquidity needs before investing.

Recurring Deposits for Regular Savings

Individuals who prefer investing small amounts every month may find Recurring Deposits (RDs) more suitable.

Most banks allow customers to start an RD with modest monthly contributions while earning interest rates comparable to fixed deposits. RDs are often preferred by students, young professionals, and first-time savers.

Government Schemes Offering Higher Returns

Apart from bank fixed deposits, investors may also consider certain government-backed savings schemes.

Senior Citizens' Savings Scheme (SCSS)

Designed specifically for eligible senior citizens, SCSS currently offers 8.2% annual interest, making it one of the highest-yielding low-risk investment options available.

Sukanya Samriddhi Yojana (SSY)

For families planning long-term savings for a girl child, the Sukanya Samriddhi Yojana also offers 8.2% annual interest, along with the benefit of long-term compounding.

Final Thoughts

Fixed deposits continue to remain a preferred investment choice for individuals seeking stable and predictable returns. While AU Small Finance Bank currently offers the highest interest rates among the banks compared, investors should also consider factors such as safety, liquidity, tenure flexibility, and overall financial goals before making an investment decision.

Disclaimer: Interest rates mentioned are based on information available in July 2026 and may change periodically. Investors should verify the latest FD rates, terms, and conditions directly with the respective bank before investing.