UTILITY

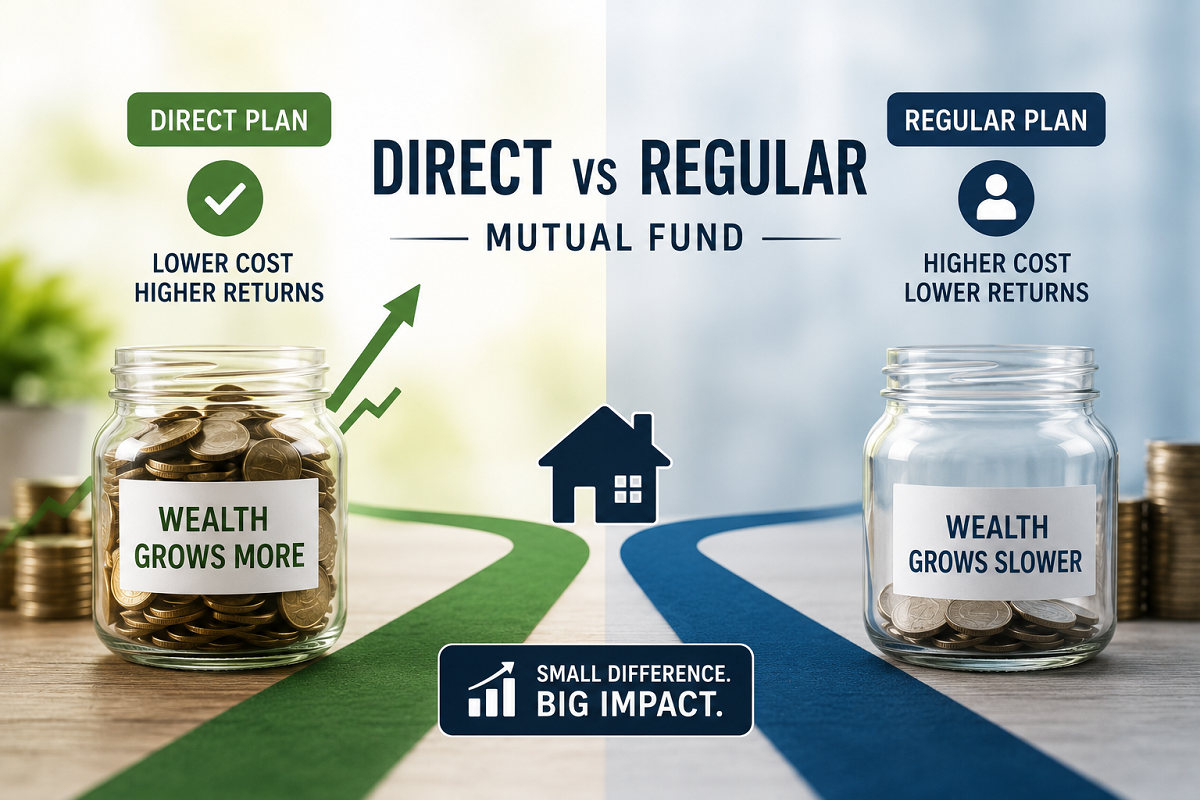

Direct vs Regular Mutual Funds: How a Small Fee Difference Can Potentially Add ₹50 Lakh to Your Wealth

Direct plans have lower costs, while regular plans offer professional guidance. Here's how the choice can impact your long-term returns.

When investing in mutual funds, every investor eventually faces one important decision—should they choose a Direct Plan or a Regular Plan?

Although both options invest in the same mutual fund scheme and are managed by the same fund manager, the returns generated over the long term can differ significantly. The key reason is the expense ratio, which represents the annual cost charged for managing the fund.

Recently, the discussion around Direct versus Regular mutual funds has gained momentum after several investment platforms introduced advisory-based mutual fund services. While some experts believe Direct Plans are the most cost-efficient option for informed investors, others argue that professional financial guidance can often justify the additional expense charged in Regular Plans.

Here's a detailed look at how both options work and which one may suit your investment style.

What Is the Difference Between Direct and Regular Mutual Funds?

The biggest distinction between the two lies in how the investment is made.

Direct Mutual Fund Plan

In a Direct Plan, investors purchase units directly from the Asset Management Company (AMC). Since there is no distributor or intermediary involved, no commission is paid.

As a result:

-

Lower expense ratio

-

Higher net returns over time

-

Suitable for self-directed investors

Regular Mutual Fund Plan

In a Regular Plan, investments are made through a financial advisor, broker, or distributor.

The AMC pays commission to the intermediary, and that cost becomes part of the expense ratio.

This means:

-

Slightly higher annual expenses

-

Access to professional investment advice

-

Portfolio review and ongoing guidance

Both plans invest in exactly the same portfolio. The difference comes only from the annual charges deducted from returns.

Why Does the Expense Ratio Matter?

At first glance, the difference between Direct and Regular Plans may appear insignificant.

In many mutual funds, the expense ratio differs by only 0.50% to 1% annually.

However, investing is driven by the power of compounding.

A seemingly small annual cost difference continues to reduce returns every year, and over decades, this can translate into a substantial gap in wealth creation.

How Can the Difference Grow Into ₹50 Lakh?

Consider a long-term investor who stays invested for around 30 years.

In a Regular Plan, a portion of the annual returns goes toward distributor commissions through the higher expense ratio.

In a Direct Plan, that money remains invested and continues earning returns year after year.

Because of compounding, the accumulated savings can potentially grow into ₹30 lakh to ₹50 lakh or even more, depending on:

-

Investment amount

-

Investment duration

-

Fund performance

-

Difference in expense ratio

The longer the investment horizon, the greater the impact of lower costs.

Does Lower Cost Always Mean Better Results?

Not necessarily.

Investment experts often point out that investor behaviour plays an even bigger role than fund expenses.

Many investors panic during market corrections and redeem their investments at the wrong time. Others invest aggressively when markets are already at record highs.

This behaviour reduces long-term returns and creates what financial professionals call the behaviour gap.

Even if a Direct Plan has lower costs, poor investment decisions can easily wipe out the benefit of saving on expenses.

When Is a Regular Plan a Better Choice?

Regular Plans may be suitable for investors who:

-

Need professional financial guidance

-

Are new to mutual fund investing

-

Prefer periodic portfolio reviews

-

Want help with asset allocation and rebalancing

-

Tend to react emotionally during market volatility

In such cases, paying a slightly higher expense ratio may be worthwhile if professional advice helps avoid costly investment mistakes.

Who Should Consider a Direct Plan?

Direct Plans are generally ideal for investors who:

-

Understand mutual fund investing

-

Can research funds independently

-

Have a disciplined long-term investment approach

-

Stay invested during market fluctuations

-

Do not require regular advisory support

These investors can benefit from lower expenses and potentially higher long-term returns.

Factors to Consider Before Choosing

Before selecting between Direct and Regular Plans, ask yourself:

-

Do I understand mutual funds well?

-

Can I manage my portfolio without professional help?

-

Will I stay invested during market downturns?

-

Do I need ongoing financial planning or guidance?

The answers to these questions are often more important than simply comparing expense ratios.

Final Takeaway

Direct and Regular Mutual Funds invest in the same underlying scheme, but the cost structure differs. A lower expense ratio in Direct Plans can generate significantly higher wealth over long investment periods due to the power of compounding.

However, the right choice depends on your investing experience, financial discipline, and ability to manage your portfolio independently. Investors comfortable making their own decisions may benefit from Direct Plans, while those seeking expert guidance may find greater value in Regular Plans despite the higher annual costs.

Disclaimer: This article is intended for informational purposes only and should not be treated as investment advice. Mutual fund investments are subject to market risks. Investors should read all scheme-related documents carefully and consult a qualified financial advisor before making investment decisions.