BUSINESS

PPF vs. EPF: Which is better for investment? Read full details on rules, interest rates, and tax exemptions

If you're a small investor, you might be confused about PPF and EPF. Today, we'll explain the difference between the two

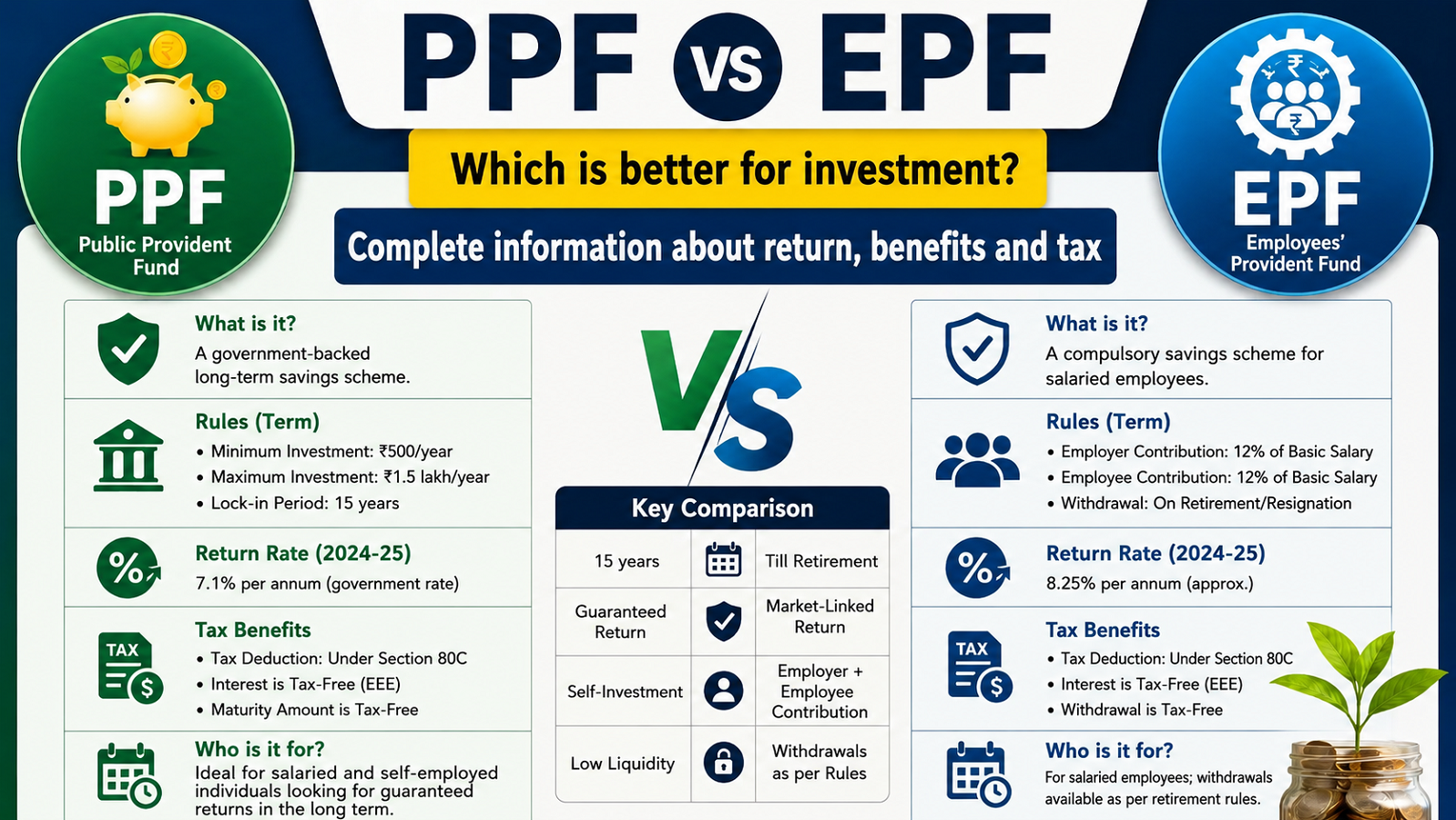

PPF vs EPF : The Public Provident Fund (PPF) and the Employees' Provident Fund (EPF) are two popular investment options used for long-term savings in India. EPF is primarily for salaried employees and is linked to their job. PPF, on the other hand, is a voluntary scheme in which anyone can invest by opening an account. While both schemes offer tax exemptions and fixed interest rates set by the government, eligibility is different. Let's understand the differences between these two investment schemes.

Public Provident Fund (PPF)

PPF is a government-backed savings scheme that guarantees tax exemption on investments, maturity amount, and interest earned (also known as EEE benefits). It has a fixed quarterly interest rate of 7.1%. It is considered one of the safest investment options for retirement and tax planning in India, especially if you are a conservative or risk-averse investor. Any post office, government bank, and some private banks in India offer PPF account opening, with a minimum monthly deposit of ₹100-500. KYC is required. Individuals can invest up to ₹1.5 lakh annually in PPF.

Its lock-in period is 15 years. After this period, you can either withdraw your deposited funds and the interest earned on them, or extend the term of the scheme as many times as you wish, in blocks of 5 years each. You can extend your PPF account by making additional deposits or without making any new deposits. If you extend it without making any new deposits, the existing balance in your account will continue to earn interest for the duration of the extended term. Therefore, if someone doesn't need the money immediately but wants to continue to benefit from tax-free compounding, extending this scheme can be an excellent option.

Employees Provident Fund (EPF)

EPF is managed by the Employees' Provident Fund Organisation (EPFO) under the EPF Act of 1952. While PPF is available to all Indian citizens, EPF is available only to salaried individuals. This scheme is run by joint contributions from both the employer and the employee, and the entire accumulated amount is paid out in one go at the time of retirement. This scheme is mainly applicable to salaried individuals working in the organised sector. The current interest rate of EPF is 8.25% per annum, which is higher than the rate of PPF and equal to the rate offered under Voluntary Provident Fund (VPF).

Under Section 80C of the old tax system, employee contributions up to ₹1.5 lakh per year are tax-deductible. Employer contributions up to 12% are tax-deductible in both the old and new tax systems.

PC:Times Now