BUSINESS

₹500 vs ₹1,000 SIP: See How a Small Monthly Difference Can Create a Huge Wealth Gap in 20 and 30 Years

Many first-time investors believe that building substantial wealth requires investing large sums every month. However, the success of a Systematic Investment Plan (SIP) depends far more on consistency and the power of compounding than on the amount you invest initially.

Even increasing your monthly SIP contribution by just ₹500 can make a significant difference over the long term. A comparison between a ₹500 SIP and a ₹1,000 SIP over 20 and 30 years shows how small, disciplined investments can grow into sizeable wealth when given enough time.

Disclaimer: The calculations below are illustrative and assume a hypothetical annual return of 12%. Mutual fund investments are subject to market risks, and actual returns may vary.

Why SIP Works for Long-Term Wealth Creation

A SIP allows investors to contribute a fixed amount at regular intervals, usually every month, into a mutual fund. Over time, the invested money benefits from the power of compounding, where returns generated on the investment also begin earning returns.

This means that staying invested for a longer period often has a greater impact on wealth creation than simply investing a larger amount for a shorter duration.

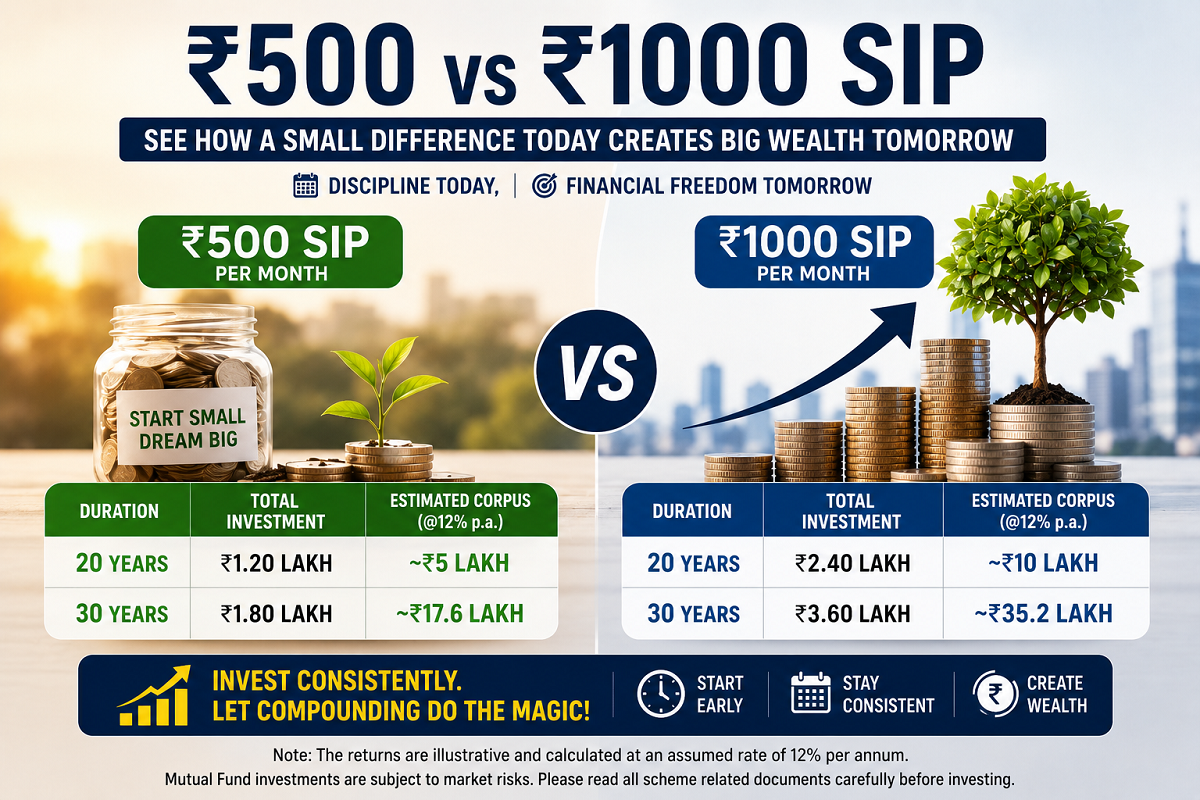

₹500 vs ₹1,000 SIP After 20 Years

Consider two investors, Rahul and Priya, who invest in the same mutual fund and earn an assumed annual return of 12%.

Rahul invests ₹500 every month for 20 years.

-

Monthly SIP: ₹500

-

Total Investment: ₹1.20 lakh

-

Estimated Corpus: Around ₹5 lakh

Priya invests ₹1,000 every month over the same period.

-

Monthly SIP: ₹1,000

-

Total Investment: ₹2.40 lakh

-

Estimated Corpus: More than ₹10 lakh

Although Priya invests only ₹500 more each month than Rahul, the larger investment, combined with compounding, results in a significantly higher final corpus after two decades.

Extending the Investment to 30 Years

The impact of compounding becomes even more noticeable when the investment period is extended.

₹500 Monthly SIP for 30 Years

If Rahul continues investing ₹500 every month for 30 years:

-

Total Investment: ₹1.80 lakh

-

Estimated Corpus: Around ₹17.6 lakh

Without increasing his monthly contribution, his investment grows to more than three times the corpus accumulated after 20 years.

₹1,000 Monthly SIP for 30 Years

If Priya continues her ₹1,000 monthly SIP for 30 years:

-

Total Investment: ₹3.60 lakh

-

Estimated Corpus: Around ₹35.2 lakh

This example demonstrates how an additional 10 years of disciplined investing can dramatically increase long-term wealth through compounding.

Time Matters More Than the Starting Amount

One of the biggest lessons from this comparison is that delaying investments can be more expensive than starting with a smaller amount.

Students, young professionals, or individuals with limited budgets do not necessarily need to wait until they can invest larger sums. Beginning with ₹500 per month can establish a healthy investment habit while allowing compounding to work over the years.

Starting early often proves more valuable than postponing investments while waiting for a higher income.

Consider Increasing Your SIP Gradually

If investing ₹1,000 every month is not currently affordable, investors can consider a step-up SIP strategy.

For example, someone starting with ₹500 per month can increase the investment by 10% every year:

-

Year 1: ₹500

-

Year 2: ₹550

-

Year 3: ₹605

Gradually increasing the SIP amount as income grows can significantly enhance long-term returns without putting excessive pressure on monthly finances.

Which SIP Amount Should You Choose?

The right SIP amount depends on your financial goals, monthly income, and ability to invest consistently.

A ₹1,000 SIP has the potential to build a substantially larger retirement or wealth corpus over time. However, if your current budget only allows ₹500, beginning your investment journey today may be more beneficial than postponing it.

Consistency, patience, and regular investing remain the key drivers of long-term wealth creation.

Disclaimer

The return figures used in this article are illustrative examples based on assumed annual returns and are not guaranteed. Mutual fund investments are subject to market risks. Investors should read all scheme-related documents carefully and consult a qualified financial advisor before making investment decisions.