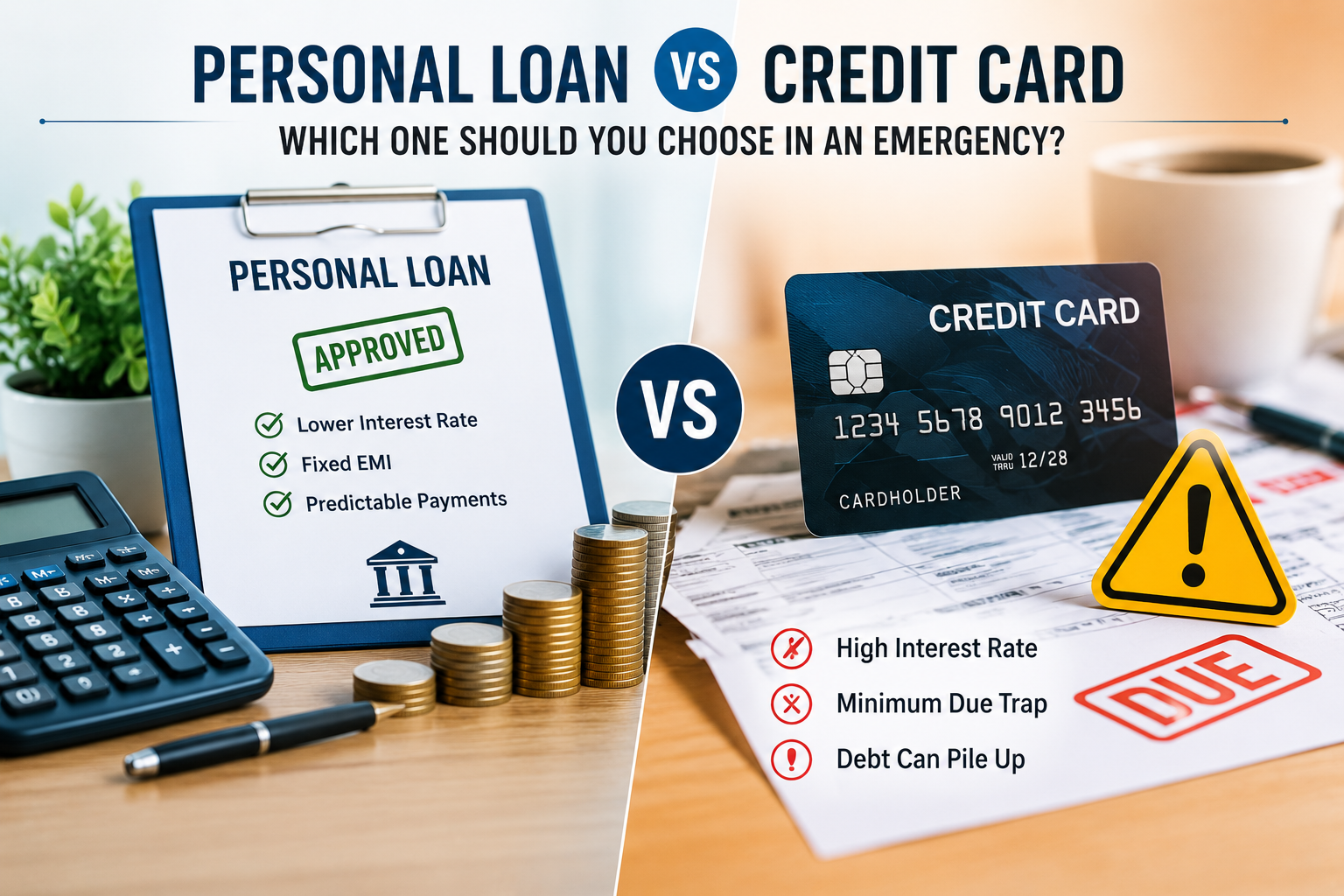

Need urgent cash? Here's how to decide between a personal loan and a credit card without paying unnecessary interest

Unexpected expenses can arise at any time. A medical emergency, urgent home repairs, temporary job loss, or any unforeseen financial situation may require immediate access to funds. In such cases, many people rely on either a personal loan or a credit card.

While both options provide quick financial support, they work very differently. Choosing the wrong option could significantly increase your borrowing cost. Understanding how each works can help you make a smarter financial decision based on your repayment ability and the amount you need.

Understanding the Difference

A personal loan is a fixed-term loan offered by banks and financial institutions. The borrower receives a lump sum and repays it through fixed monthly EMIs over a pre-decided period.

A credit card, on the other hand, allows users to spend up to a sanctioned credit limit. If the full outstanding amount is paid before the due date, interest is generally not charged. However, carrying forward unpaid balances can attract very high interest rates.

Example: Borrowing ₹2 Lakh for an Emergency

Suppose you suddenly need ₹2 lakh to cover hospital expenses.

Option 1: Personal Loan

Assume a bank offers a ₹2 lakh personal loan at an annual interest rate of 12% for three years.

| Details | Amount |

|---|---|

| Loan Amount | ₹2,00,000 |

| Interest Rate | 12% per annum |

| Loan Tenure | 3 Years |

| Approximate EMI | ₹6,640 |

| Total Repayment | Around ₹2.39 lakh |

| Total Interest Paid | Around ₹39,000 |

The biggest advantage is predictability. Your EMI remains fixed throughout the loan tenure, making budgeting easier.

Option 2: Credit Card

Now imagine you pay the entire ₹2 lakh using your credit card but repay only the minimum amount due each month.

Most credit cards charge interest ranging between 30% and 48% annually if the outstanding balance is not paid in full. Additional charges and GST may also apply depending on the issuer's terms.

As a result, the unpaid balance continues to accumulate interest every month, making the borrowing cost substantially higher than a personal loan.

Personal Loan vs Credit Card: Quick Comparison

| Feature | Personal Loan | Credit Card |

|---|---|---|

| Interest Rate | Around 10%–18% annually | Around 30%–48% annually |

| Repayment | Fixed EMIs | Minimum due or full payment |

| Best For | Large expenses | Short-term borrowing |

| Cost | Lower for long-term repayment | Can become expensive if balance is carried forward |

When Is a Credit Card the Better Choice?

A credit card works well if:

-

You need money for a short period.

-

You can repay the entire outstanding amount within the interest-free period.

-

The expense is relatively small.

For example, if you pay a ₹50,000 hospital bill using your credit card and clear the full amount before the due date, you can usually avoid paying any interest.

When Should You Choose a Personal Loan?

A personal loan is generally more suitable if:

-

You need a large amount.

-

Repayment will take several months or years.

-

You prefer predictable monthly EMIs.

-

You want to avoid high revolving credit card interest.

Expenses such as medical treatment, weddings, home renovation, or emergency family needs often make a personal loan a more economical option.

How Big Can the Difference Be?

Consider borrowing ₹1 lakh.

If you finance it through a credit card and continue paying only the minimum due, interest and other charges could add ₹30,000–₹40,000 or more over time, depending on repayment behaviour and card terms.

In comparison, a ₹1 lakh personal loan at 12% annual interest for three years would result in:

-

Approximate EMI: ₹3,320

-

Total repayment: Around ₹1.20 lakh

-

Total interest: Approximately ₹20,000

This example highlights how a structured loan can significantly reduce borrowing costs when repayment extends beyond a few weeks.

Build an Emergency Fund to Reduce Borrowing

Financial experts recommend maintaining an emergency fund equal to at least six months of essential expenses. Having emergency savings can reduce or eliminate the need to rely on costly debt during unexpected situations.

Final Takeaway

Both personal loans and credit cards have their place in financial planning. The right choice depends on how much money you need and how quickly you can repay it.

-

Choose a credit card if you are confident you can clear the entire bill within the interest-free period.

-

Choose a personal loan for larger expenses or when repayment will be spread over several months or years.

Before borrowing, compare interest rates, processing charges, repayment terms, and your own financial capacity. Careful planning can help you manage emergencies without placing unnecessary pressure on your finances.

Disclaimer: This article is intended for informational purposes only and should not be considered financial advice. Loan terms, interest rates, and credit card charges vary across lenders. Always compare available options and consult a qualified financial advisor before making borrowing decisions.