BUSINESS

New EPF Rules 2026 Explained: How the Revised Contribution Limit Could Change Your Take-Home Salary

The Government of India has implemented the Employees' Provident Fund (EPF) Scheme, 2026 under the Social Security Code, 2020, introducing significant changes to the mandatory provident fund contribution structure. The revised framework came into effect on June 29, 2026, replacing the earlier contribution mechanism for eligible employees and employers.

The update has sparked widespread interest among salaried employees, particularly regarding its impact on monthly take-home pay and long-term retirement savings. While some employees may notice an increase in their in-hand salary, financial experts caution that the long-term effect on retirement planning should not be overlooked.

What Has Changed Under the New EPF Rules?

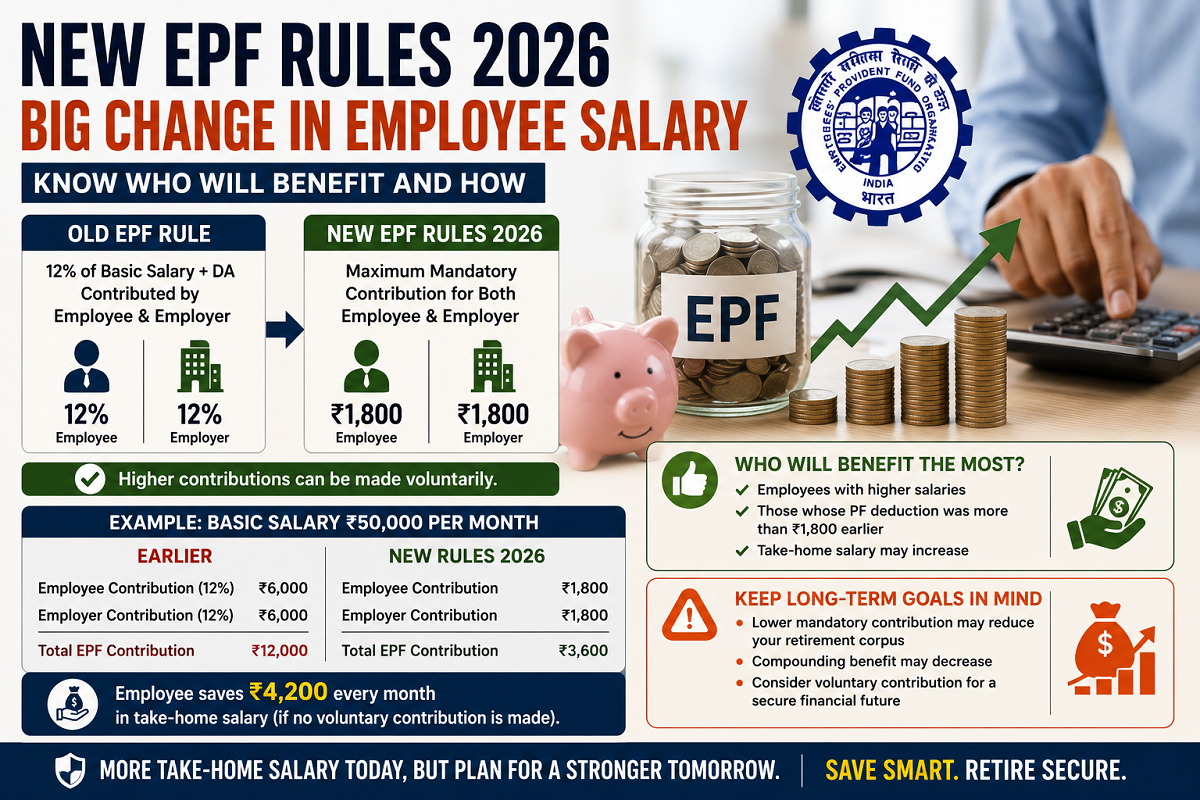

Under the previous EPF system, both the employee and employer generally contributed 12% of the employee's basic salary plus dearness allowance (DA) toward the EPF account. As salaries increased, the mandatory PF contribution also increased proportionately.

Under the EPF Scheme 2026, the mandatory monthly EPF contribution has been capped at ₹1,800 each for both the employer and the employee.

However, employees and employers who wish to contribute more than the mandatory limit may still do so through voluntary contributions, subject to applicable EPF provisions.

How Could the New Rule Affect Your Take-Home Salary?

The impact of the revised contribution structure depends largely on an employee's salary and the employer's compensation structure.

According to tax and payroll professionals, employees whose mandatory PF deductions previously exceeded ₹1,800 per month could experience a higher monthly take-home salary if they choose not to make additional voluntary EPF contributions.

Since a smaller amount would now be deducted as the mandatory employee contribution, more money may remain in the employee's monthly salary.

However, the final impact varies depending on factors such as:

-

The employee's Cost to Company (CTC) structure

-

Employer payroll policies

-

Whether voluntary EPF contributions are continued

-

Individual salary components

Understanding the Change with an Example

Consider an employee with a basic salary of ₹50,000 per month.

Under the Earlier EPF Structure

-

Employee contribution (12%): ₹6,000

-

Employer contribution (12%): ₹6,000

-

Total monthly EPF contribution: ₹12,000

Under the New EPF Scheme 2026

-

Mandatory employee contribution: ₹1,800

-

Mandatory employer contribution: ₹1,800

-

Total mandatory monthly EPF contribution: ₹3,600

In this illustration, the employee's monthly deduction falls from ₹6,000 to ₹1,800, leaving approximately ₹4,200 more in monthly take-home pay, provided no additional voluntary contribution is made.

Actual salary outcomes may differ depending on the employer's compensation policies and payroll design.

Which Employees Are Likely to Benefit the Most?

The revised contribution cap is expected to have the greatest impact on employees with relatively higher salaries.

Previously, employees earning higher basic salaries contributed significantly larger amounts toward EPF due to the percentage-based calculation. Under the revised framework, a larger portion of those contributions may now become voluntary instead of mandatory.

Employees whose PF deductions were already close to ₹1,800 per month are unlikely to see a significant difference in their monthly salary.

Higher Salary Today Could Mean Lower Retirement Savings Tomorrow

Although a higher in-hand salary may appear financially beneficial in the short term, financial planners advise employees to carefully consider the long-term consequences.

A lower mandatory EPF contribution means that less money is invested in the retirement corpus unless the employee voluntarily continues contributing additional amounts.

Over several decades, this may reduce the benefits of compound interest, resulting in a smaller retirement fund compared to the previous contribution structure.

Employees who prioritize long-term financial security may therefore consider maintaining higher voluntary EPF contributions even if the mandatory deduction has decreased.

Should You Increase Voluntary Contributions?

Whether to contribute beyond the mandatory limit depends on your financial goals, current expenses, investment strategy, and retirement planning.

Employees should evaluate factors such as:

-

Long-term retirement requirements

-

Monthly cash flow needs

-

Other investment options

-

Risk tolerance

-

Existing retirement savings

Consulting a qualified financial advisor can help determine whether continuing higher EPF contributions aligns with individual financial objectives.

Key Takeaway

The EPF Scheme 2026 changes the way mandatory provident fund contributions are calculated, potentially increasing take-home salaries for many higher-income employees. However, the reduction in compulsory retirement savings could also reduce long-term wealth accumulation if additional voluntary contributions are not maintained.

Before making any financial decisions based on the revised rules, employees should review their salary structure, retirement goals, and investment plans to ensure they maintain an appropriate balance between present income and future financial security.