BUSINESS

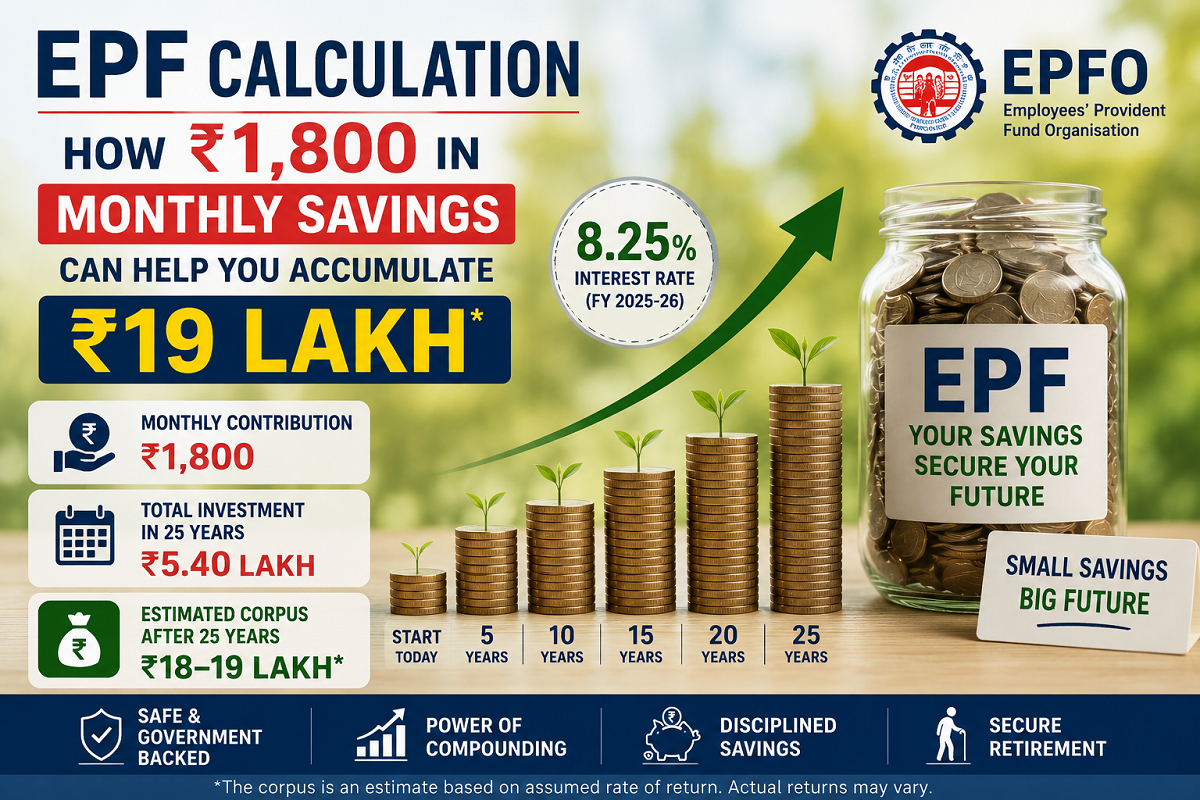

EPF Calculator: How a ₹1,800 Monthly Contribution Can Grow Into Nearly ₹19 Lakh Over 25 Years

EPF Calculation Explained: The Power of Small Monthly Savings and Compounding for Long-Term Retirement Wealth

Many salaried employees believe that building a large retirement corpus requires a high income or substantial monthly investments. However, consistent contributions to the Employees' Provident Fund (EPF) can help create significant long-term wealth even with modest monthly savings.

The Employees' Provident Fund Organisation (EPFO) manages the EPF scheme, which is one of India's most popular retirement savings programmes for salaried workers. Besides encouraging disciplined savings, the scheme offers annual interest that helps the accumulated balance grow steadily over time through the power of compounding.

For employees who stay invested throughout their career, even a relatively small monthly contribution can translate into a sizeable retirement fund.

How EPF Supports Long-Term Financial Security

EPF is designed to help employees build a retirement corpus through regular monthly contributions made by both the employee and the employer. The accumulated amount earns annual interest, which is credited to the account and becomes part of the principal for future interest calculations.

For FY 2025-26, the EPF interest rate has been fixed at 8.25% per annum, enabling members to benefit from long-term compounding.

Unlike many short-term savings options, EPF encourages disciplined investing over several decades, allowing the retirement corpus to grow without requiring active management from the employee.

Understanding the Power of Compounding

Compounding plays a crucial role in wealth creation through EPF.

Instead of earning interest only on the original contributions, members also earn interest on the interest accumulated in previous years. As the investment period becomes longer, this compounding effect accelerates the growth of the retirement corpus.

The longer the money remains invested, the greater the benefit of compound interest.

EPF Calculation: ₹1,800 Monthly Contribution

Let's understand the calculation using a simple example.

Assumptions

-

Monthly EPF contribution: ₹1,800

-

Annual contribution: ₹21,600

-

Investment period: 25 years

-

EPF interest rate: 8.25% per annum

Estimated Outcome

| Particulars | Amount |

|---|---|

| Monthly Contribution | ₹1,800 |

| Annual Contribution | ₹21,600 |

| Total Investment (25 Years) | ₹5.40 lakh |

| Estimated Retirement Corpus | Nearly ₹18–19 lakh* |

*The estimated corpus is based on the assumed contribution period and prevailing EPF interest rate. Actual returns may vary depending on annual interest rates, salary revisions, and contribution changes.

Why the Final Amount Is Much Higher

Although the employee contributes only ₹5.40 lakh over 25 years, the retirement corpus grows to nearly ₹19 lakh because interest continues to accumulate every year.

This illustrates how time can become one of the most valuable factors in long-term investing. Starting early and remaining consistent often has a greater impact than making occasional large investments.

Benefits of Investing Through EPF

EPF remains one of the preferred retirement savings options for salaried employees because it offers several advantages:

-

Regular monthly savings through salary deductions.

-

Government-backed retirement savings framework.

-

Annual interest credited to the accumulated balance.

-

Compounding helps accelerate long-term wealth creation.

-

Tax benefits are available under applicable provisions of the Income Tax Act, subject to the chosen tax regime and prevailing rules.

-

Encourages disciplined retirement planning without requiring frequent investment decisions.

Ways to Build an Even Larger Retirement Corpus

Employees looking to increase their retirement savings may consider:

-

Increasing EPF contributions whenever salary increases.

-

Making voluntary contributions through the Voluntary Provident Fund (VPF), where eligible.

-

Remaining invested for a longer working career.

-

Avoiding premature EPF withdrawals unless absolutely necessary.

-

Reviewing retirement goals periodically and supplementing EPF with other long-term investment options such as NPS or mutual funds.

Why Starting Early Matters

One of the biggest advantages of EPF is that it rewards consistency rather than large one-time investments. Employees who begin contributing early in their careers give their investments more time to compound, resulting in a significantly larger retirement corpus.

Even modest monthly contributions can grow substantially when invested over two or three decades, making EPF an important pillar of long-term financial planning for salaried individuals.

Disclaimer: The above calculation is for illustrative purposes only and is based on assumed contributions and the prevailing EPF interest rate. Actual maturity value may vary depending on salary revisions, contribution amounts, interest rate changes, and EPFO guidelines. Employees should refer to official EPFO rules or consult a financial advisor before making retirement planning decisions.