BUSINESS

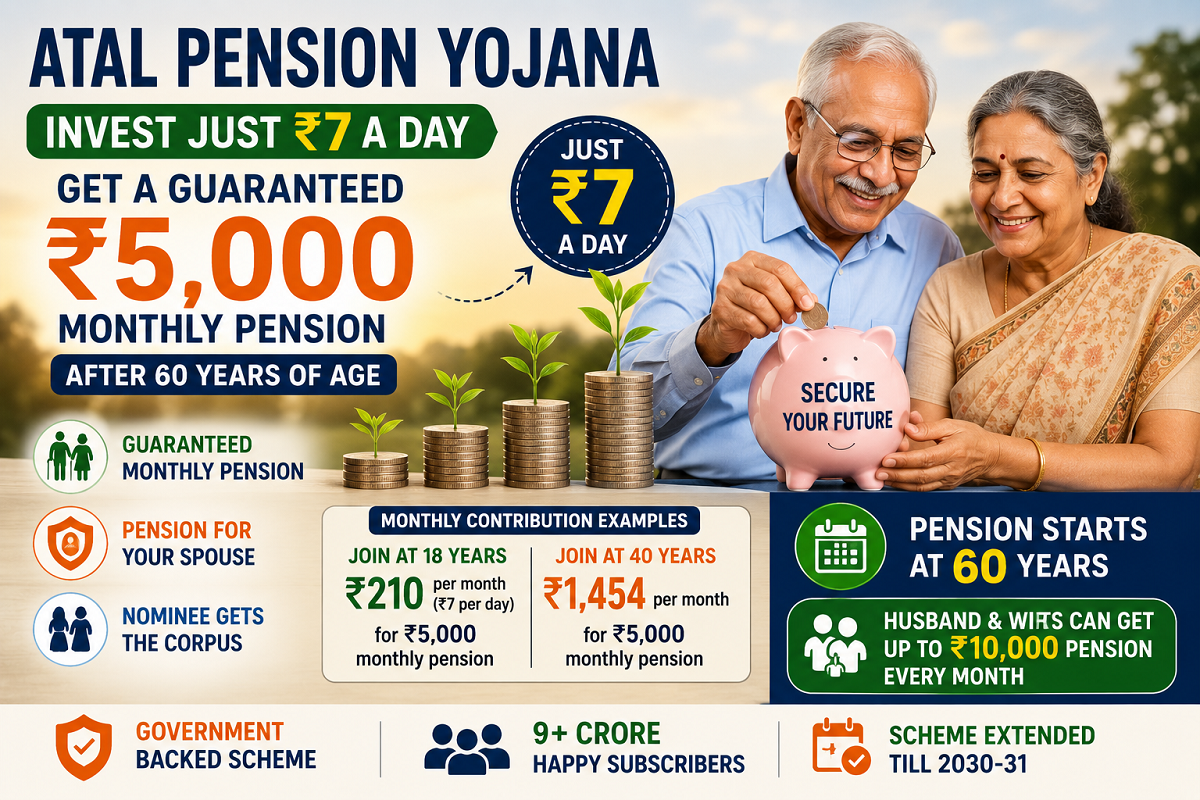

Atal Pension Yojana: Invest Around ₹7 a Day and Receive Up to ₹5,000 Monthly Pension After 60

APY Explained: Eligibility, Contribution, Pension Benefits and How Early Enrollment Can Reduce Your Investment

Planning for retirement at a young age can significantly improve financial security in later years. One of the government's most affordable retirement schemes, the Atal Pension Yojana (APY), allows eligible individuals to build a guaranteed pension through small, regular contributions.

Introduced to encourage retirement savings among workers in the unorganised sector, APY has become one of India's most widely adopted pension programmes. The scheme is backed by the Government of India and provides subscribers with a fixed monthly pension after they attain the age of 60.

With the scheme now extended until 2030-31 and total enrolment crossing 9 crore subscribers, APY continues to attract millions of individuals seeking a reliable retirement income.

What Is Atal Pension Yojana?

Launched in 2015, the Atal Pension Yojana is a government-supported pension scheme that helps eligible citizens accumulate retirement savings through affordable monthly contributions.

The biggest attraction of APY is its guaranteed pension, which ranges from ₹1,000 to ₹5,000 per month, depending on the contribution selected at the time of enrolment.

Since the pension amount is backed by the government, many investors consider APY a dependable option for long-term retirement planning.

Who Can Join APY?

Individuals must satisfy the following eligibility conditions to open an APY account:

-

Be an Indian citizen.

-

Be between 18 and 40 years of age.

-

Have an active savings account with a bank or post office.

-

Not be an income-tax payer at the time of opening a new APY account.

As per the rules effective from October 1, 2022, individuals who are or have been income-tax payers are not eligible to open a new APY account. However, subscribers who joined before this date continue to receive all applicable scheme benefits.

Major Benefits of Atal Pension Yojana

Guaranteed Monthly Pension

After attaining the age of 60 years, subscribers receive a fixed monthly pension based on the contribution plan chosen during enrolment.

Available pension options include:

-

₹1,000 per month

-

₹2,000 per month

-

₹3,000 per month

-

₹4,000 per month

-

₹5,000 per month

Lifetime Pension for the Spouse

In the event of the subscriber's death after pension commencement, the spouse continues to receive the same monthly pension for life, ensuring financial stability for the surviving family member.

Nominee Receives the Pension Corpus

After the death of both the subscriber and the spouse, the accumulated pension corpus is transferred to the registered nominee according to the scheme rules.

How Much Do You Need to Contribute?

The monthly contribution depends on the subscriber's age at the time of joining. Younger subscribers contribute lower amounts because they invest for a longer period.

If You Join at 18 Years

| Pension Option | Monthly Contribution |

|---|---|

| ₹5,000 Monthly Pension | ₹210 (about ₹7 per day) |

| ₹1,000 Monthly Pension | ₹42 |

If You Join at 40 Years

| Pension Option | Monthly Contribution |

|---|---|

| ₹5,000 Monthly Pension | ₹1,454 |

| ₹1,000 Monthly Pension | ₹291 |

The comparison clearly shows that starting early allows investors to secure a higher retirement pension with much smaller monthly contributions.

Couples Can Receive Up to ₹10,000 Every Month

One of the attractive features of APY is that both husband and wife can open separate APY accounts, provided they individually satisfy the eligibility criteria.

If both subscribe to the maximum pension option of ₹5,000 each, the household can receive a combined pension of ₹10,000 per month after retirement.

Pension Starts at Age 60

Subscribers become eligible to receive pension benefits after completing 60 years of age.

To qualify for pension payments, contributions must continue for a minimum of 20 years. For example, someone enrolling at age 40 will contribute until age 60 before the pension begins.

Withdrawal Rules

The scheme is primarily intended for long-term retirement planning and generally discourages premature withdrawals.

Key rules include:

-

Early exit is usually permitted only in cases such as terminal illness or the subscriber's death.

-

Voluntary closure before maturity allows withdrawal of personal contributions along with applicable interest.

-

Any government co-contribution, wherever applicable under earlier provisions, may not be payable upon voluntary exit.

Why APY Continues to Grow

Crossing the milestone of 9 crore subscribers reflects the growing acceptance of APY among low- and middle-income households.

The scheme's affordability, government-backed pension guarantee, family protection benefits, and simple enrolment process have made it one of India's leading retirement savings programmes. Participation by women has also increased steadily, further strengthening its reach across households.

Final Takeaway

The Atal Pension Yojana offers an affordable path to building a guaranteed retirement income. Individuals who begin investing at a younger age can secure a ₹5,000 monthly pension by contributing as little as ₹210 per month, or roughly ₹7 per day.

For those seeking a predictable pension after retirement, APY remains a practical long-term savings option, particularly for eligible individuals working outside the organised pension system.

Disclaimer: Scheme rules, eligibility conditions, and contribution amounts are subject to government notifications and applicable regulations. Prospective subscribers should verify the latest guidelines with their bank or the official APY portal before enrolling.