BUSINESS

Personal Loan Rejected? It's Not Just Your Credit Score—5 Other Factors Banks Carefully Evaluate

A personal loan can provide quick financial support during emergencies, medical expenses, home repairs, education costs, or other unexpected needs. However, receiving a loan rejection can be frustrating, especially if you believe your income is stable and your repayment capacity is strong.

Many borrowers assume that a low credit score is the only reason a lender declines a loan application. In reality, banks and financial institutions evaluate several aspects of an applicant's financial profile before making a lending decision.

Even applicants with good credit scores may face rejection if other risk factors raise concerns. Here are five important reasons why your personal loan application may not be approved.

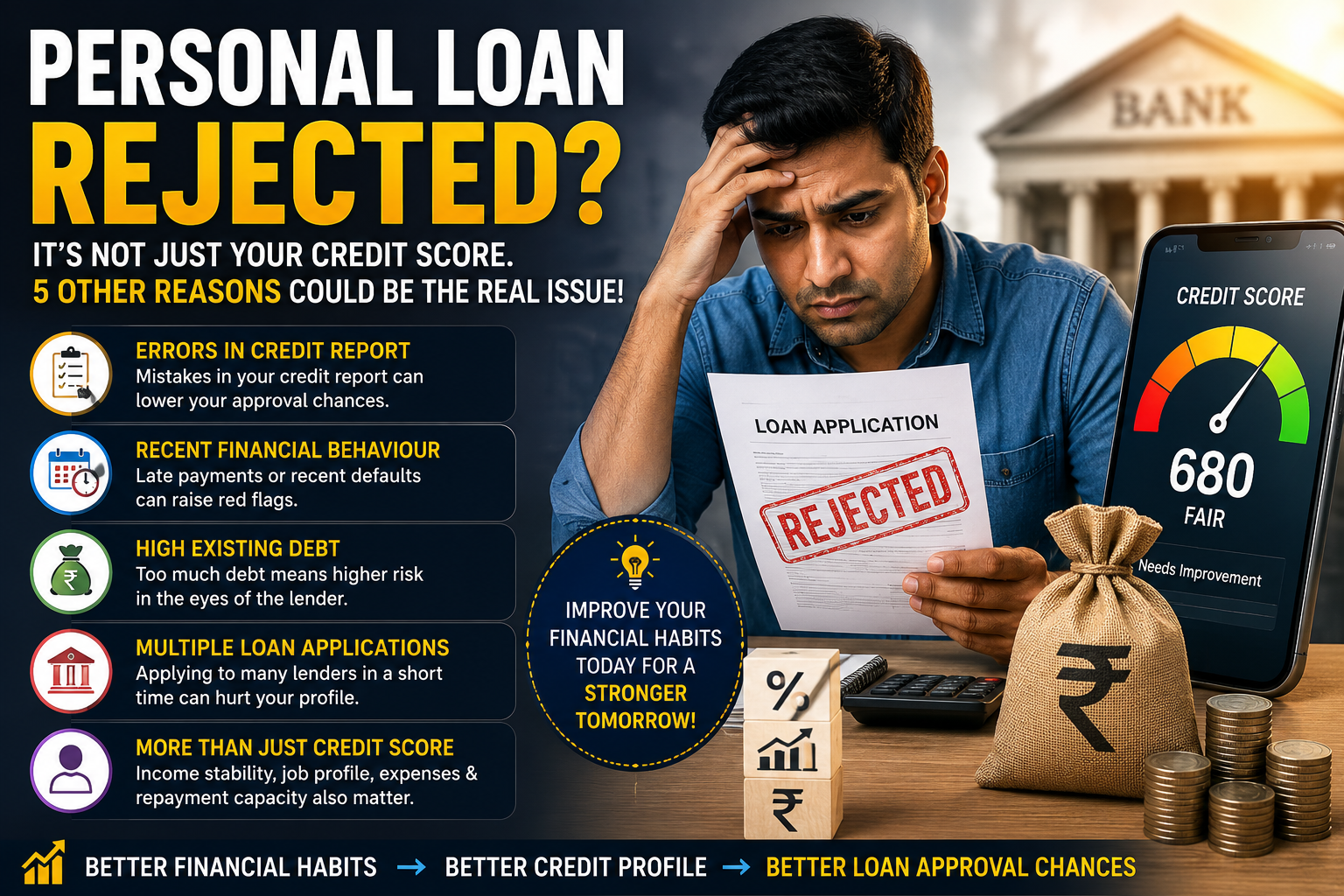

1. Errors in Your Credit Report Can Affect Approval

Your credit report plays a major role in the loan evaluation process, but it is important to ensure the information it contains is accurate.

Loan approval can be affected by issues such as:

-

Incorrect loan records.

-

Payments marked as delayed despite timely repayment.

-

Closed loans still appearing as active.

-

Incorrect personal information.

-

Reporting errors by lenders.

Before applying for a new loan, review your credit report carefully and request corrections if you notice any inaccuracies.

2. Recent Financial Behaviour Matters

Banks don't evaluate only your long-term credit history—they also pay close attention to your recent financial conduct.

Lenders often assess whether you have:

-

Paid recent EMIs on time.

-

Cleared credit card bills regularly.

-

Maintained disciplined repayment habits.

-

Avoided recent payment defaults.

Even if you experienced financial difficulties several years ago, a consistent repayment record over the recent months can strengthen your loan application.

Conversely, recent missed or delayed payments may reduce your approval chances, even with an otherwise satisfactory credit score.

3. Existing Debt Can Reduce Eligibility

Another important factor is your current debt burden.

Banks generally examine how much of your monthly income is already committed toward existing loan repayments.

If a significant portion of your salary is being used to pay:

-

Home loan EMIs.

-

Vehicle loans.

-

Personal loans.

-

Credit card dues.

-

Other financial obligations.

the lender may conclude that taking on another loan could increase repayment risk.

Reducing outstanding debt before applying for another loan may improve your eligibility.

4. Applying to Multiple Banks Within a Short Period

Many applicants submit loan applications to several lenders immediately after receiving one rejection.

However, multiple loan enquiries within a short period may signal financial stress to lenders.

Every loan application can generate a credit enquiry, and numerous enquiries in a limited timeframe may negatively influence lending decisions.

Instead of submitting repeated applications, it is generally better to identify the reason for the earlier rejection, improve your financial profile, and then apply again.

5. Credit Score Alone Does Not Decide Approval

Two individuals with similar credit scores may still receive different lending decisions.

This is because banks also evaluate several additional factors, including:

-

Employment stability.

-

Regularity of income.

-

Employer profile.

-

Existing liabilities.

-

Debt-to-income ratio.

-

Repayment behaviour.

-

Overall financial discipline.

A strong and consistent financial profile often carries as much importance as the credit score itself.

What Should You Do If Your Loan Is Rejected?

A rejected application does not necessarily mean future loans will also be declined.

You can improve your borrowing profile by taking practical steps such as:

-

Paying EMIs on or before their due dates.

-

Clearing outstanding credit card balances.

-

Reducing existing debt.

-

Correcting errors in your credit report.

-

Avoiding unnecessary loan applications.

-

Maintaining a healthy credit utilisation ratio.

These measures may gradually strengthen your credit profile and improve your eligibility for future borrowing.

Build Your Financial Profile Before Reapplying

Rather than applying repeatedly after a rejection, borrowers should first understand why the application was declined.

Improving repayment discipline, maintaining accurate credit records, and managing existing debt responsibly can significantly enhance loan eligibility over time.

While every lender follows its own internal credit assessment policy, maintaining a stable financial profile and responsible borrowing habits generally improves the likelihood of personal loan approval in future applications.

Disclaimer: This article is intended for general informational purposes only and should not be considered financial advice. Loan approval depends on the lending institution's eligibility criteria, internal risk assessment, and applicable regulations. Borrowers should carefully review loan terms and seek professional financial advice before making borrowing decisions.